Effective April 1st, 2024, Stephen Cummings, CEO of Rizolve Partners, will step into the role of Interim CEO of Ontario Genomics (OG) on a part-time basis over the next six months. Under the direction of the OG Board of Directors and in close collaboration with company’s management team, Stephen will oversee OG’s strategic direction and support the Board in the recruitment process for the new President and CEO.

Stephen’s nine-year tenure on OG’s board, coupled with his background in strategic business advisory as CEO of Rizolve Partners and private equity/venture capital, uniquely positions him to guide OG through this transition period with a steady hand – whose mission is to lead the application of genomics-based solutions across key sectors of the economy to drive economic growth, improved quality of life and global leadership for Ontario.

We look forward to embarking on this journey together with Ontario Genomics.

In today’s competitive business landscape, the importance of customer satisfaction cannot be overstated; it is a critical factor that can make or break your company. Happy customers are more likely to become loyal patrons, refer others, and contribute to your bottom line. But how do you measure customer satisfaction? One very effective way is the Net Promoter Score® (NPS®) – a powerful metric that provides actionable insights for business owners.

In this article, we explore the crucial role of customer satisfaction and delve into the benefits of tracking your NPS as a valuable metric for gauging customer loyalty and a proven indicator of business growth or decline.

HAPPY CUSTOMERS – THE ENGINE OF SUSTAINED GROWTH

Happy customers are the driving force behind sustained business growth. Prioritizing customer satisfaction is a powerful driver of business success for numerous reasons:

→ Revenue Generation: Happy customers are more willing to spend, making repeat purchases and exploring additional offerings. A satisfied customer base directly contributes to increased sales and revenue.

→ Loyalty and Repeat Business: Satisfied customers remain loyal, choosing your products or services repeatedly. This not only boosts revenue but also reduces customer acquisition costs.

→ Competitive Edge: Prioritizing customer satisfaction sets your business apart from competitors. Exceptional service and positive experiences motivate customers to choose you over alternatives.

→ Awareness and Trust: Satisfied customers become brand ambassadors, enhancing your brand’s visibility and reputation. A strong brand presence attracts new customers and reinforces trust.

→ Brand Reputation: Customer satisfaction significantly shapes a company’s brand reputation. A positive reputation is a valuable intangible asset that differentiates a business in a crowded marketplace.

→ Word-of-Mouth Marketing: Happy customers serve as the best advocates for your business. Their positive word-of-mouth recommendations can influence potential customers more effectively than traditional marketing efforts.

→ Support During Crises: Satisfied customers provide stability during difficult times. Whether it’s a product issue, service disruption, or external crisis, their loyalty and support can make a significant difference.

→ Innovation and Feedback Loop: Satisfied customers are more likely to share insights, highlight pain points, and suggest improvements, contributing to innovation and continuous improvement.

→ Employee Morale and Productivity: Positive customer interactions boost employee morale, leading to increased productivity and commitment. Satisfied customers contribute to a virtuous cycle, benefiting employees and overall business performance.

Prioritizing customer satisfaction is not just about fulfilling customer expectations but exceeding them to foster loyalty and advocacy which fuel sustained business growth.

This is where Net Promoter Score (NPS) comes into play as a crucial metric.

WHAT IS THE NET PROMOTER SCORE?

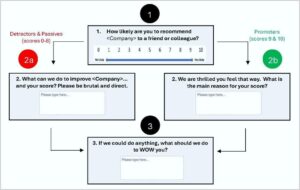

NPS measures the likelihood of customers recommending your brand to others, reflecting their overall satisfaction and loyalty. It is a potent tool that revolves around a single question: “On a scale of 0 to 10, how likely are you to recommend our product/service to a friend or colleague?”.

Based on their responses, customers are categorized as Promoters, Passives, or Detractors.

Promoters (9-10): These are your most enthusiastic and loyal customers. They actively promote your business and contribute to positive word-of-mouth marketing to help drive business growth. “They account for more than 80% of referrals in most businesses”. (Bain & Company)

Passives (7-8): Passives are satisfied but not enthusiastic. They won’t actively promote your brand but won’t discourage others either.

Detractors (0-6): Detractors are unhappy customers who are unlikely to remain patrons, and – worse – may spread negative feedback. Addressing their concerns is crucial.

NPS is calculated by subtracting the percentage of ‘Demoters’ (1-6) from the percentage of ‘Promoters’ (9-10). For example, if you have 45% Promoters, 35% Passives, and 20% Detractors, your NPS score would be 45 – 20 = 25.

While Passives are not considered in calculating the NPS score, they are extremely important because they are very close to becoming either a Promoter or a Demoter.

WHAT IS A GOOD NPS SCORE?

NPS is always expressed as a number from -100 to 100. The higher your NPS score, the more likely you are to have loyal customers who will help you grow your business.

According to Bain & Company, the following is a general rating of Net Promoter Scores:

Any score above zero is considered good because it indicates that a business has more Promoters than Detractors.

Any score above 20 is considered favourable.

Any score above 50 is considered excellent.

Any score above 80 is considered world-class.

It should be noted that what is considered a ‘good,’ ‘bad,’ or ‘neutral’ NPS can vary substantially across industries. For example, an NPS of -3 may seem quite bad, but if the industry average is -10, the score would not look as bad.

Nonetheless, any score below 0 indicates that a business has more Detractors than Promoters, and therefore needs improvement.

WHY USE NPS?

NPS is widely used by B2B and B2C businesses large and small around the world. As a business metric, NPS can be easily tracked and quantified over time, and it has proven to be a reliable predictor of future business growth or decline.

NPS enables businesses to benchmark and compare their scores to industry standards. It also helps companies organize around a crucial objective — to increase their score by earning more enthusiastic customers.

But the true power of the NPS system is asking one or two follow-up questions as part of the standard NPS survey. By asking customers why they have given the score they have, and what the business can do to improve their score, companies can understand what they’re doing well and, even more importantly, where they could be improving.

Although customer satisfaction is not the sole determinant of growth, profitable organic growth cannot be sustained without it. By understanding the factors that contribute to customer loyalty or dissatisfaction, companies can make informed decisions to enhance the customer experience.

Regularly tracking NPS allows businesses to gauge the impact of changes in products, services, or processes on customer satisfaction. This feedback loop enables continuous improvement, helping companies adapt to evolving customer expectations in an increasingly competitive marketplace.

Customer satisfaction and NPS go hand in hand. Prioritize both, and watch your business thrive. Remember, customer satisfaction is not merely a metric; it is a powerful driver of business success. Investing in and tracking customer happiness pays dividends in the long run, making it a strategic imperative for any successful company.

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth.

®Net Promoter, Net Promoter System, Net Promoter Score, NPS and the NPS-related emoticons are registered trademarks of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc.

In the world of sales, achieving success is akin to winning the Super Bowl. Just like a championship football team relies on a well-crafted playbook, sales teams benefit greatly from a strategic and comprehensive sales playbook. In this blog post, we’ll explore the parallels between coaching a Super Bowl team and creating a winning sales playbook.

Scouting the Competition: Know Your Opponents

Super Bowl-winning coaches spend countless hours studying the strengths and weaknesses of their opponents. Similarly, successful sales teams must understand their market, competitors, and potential clients.

Conduct thorough market research, analyze competitors, and identify your target audience’s pain points to create a playbook that positions your team for success.

Build a Stellar Roster: Assemble Your Dream Sales Team

A championship team is made up of skilled and diverse players. In the sales arena, hiring and training the right team members are crucial.

Your sales playbook should include a comprehensive guide on recruiting, onboarding, and continuous training to ensure your team is well-equipped to tackle any challenge.

Crafting the Perfect Game Plan: Designing Your Sales Playbook

Just like a Super Bowl team needs a well-thought-out game plan, your sales playbook should outline the entire sales process, from prospecting to closing deals.

Break down each stage, identify key plays (sales tactics), and provide guidelines for various scenarios.

A well-crafted playbook ensures that your team is prepared for any situation on the field.

Training: Preparation is Key

Before the Super Bowl, teams engage in intense practice sessions to fine-tune their skills and enhance team cohesion. Likewise, sales teams should undergo regular training sessions.

Include role-playing exercises, product knowledge refreshers, and simulated sales scenarios in your playbook to keep your team sharp and ready to perform at their best.

Adaptability: Be Ready to Call Audibles

In football, coaches often need to call audibles – changing the play at the last minute based on the opponent’s actions. Similarly, your sales playbook should encourage adaptability.

Equip your team with the skills to read clients’ signals, adjust strategies on the fly, and overcome objections effectively.

Utilizing Technology: Your Playbook’s MVP

Just as technology plays a crucial role in modern football, it is also an essential component of a successful sales playbook.

Leverage customer relationship management (CRM) tools, analytics, and other technologies to streamline processes, track performance, and gain valuable insights.

Game Day: Executing Your Plays with Precision

When the Super Bowl arrives, it’s time to execute the plays that have been rehearsed and perfected. Similarly, the real test for your sales team comes when engaging with clients.

Regularly review and update your playbook based on real-world experiences, ensuring that your team is always using the most effective plays in the field.

Winning With Your Sales Playbook

In the world of sales, building and executing a winning playbook is the key to success, much like coaching a Super Bowl team. By scouting the competition, assembling a stellar team, crafting a comprehensive game plan, and embracing adaptability and technology, your sales playbook can lead your team to victory in the competitive marketplace.

So, gear up, get ready, and let the sales Super Bowl begin!

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth. To learn more, check out our services here.

As a private business owner, you know that your employees are your most valuable asset. They are the talent who drive your business forward, deliver quality products and services, and satisfy your customers. Having the right people in the right roles can propel results and define a company’s competitive edge, and “is an essential imperative that is critical for business success”, according to Sue Cummings, former head of HR at TD Bank Group. However, finding, developing, and keeping the right talent can be challenging, especially in a competitive and dynamic market. That is why you need a talent management strategy.

Outlined below are the key elements of a talent management strategy, many of which are often overlooked by Management who relegate some of these components as “peripheral”. Sue believes that “this is a mistake because having a plan to step into an increasingly mature approach over time is a key business value driver – and one that is scrutinized by third parties during a liquidity event”.

WHAT IS A TALENT MANAGEMENT STRATEGY?

A talent management strategy is a plan that outlines how you will attract, develop, and retain your workforce. It is aligned with your vision, mission, values, and goals, and drives your competitive advantage.

WHY A TALENT MANAGEMENT STRATEGY IS IMPORTANT

In the dynamic and competitive landscape of today’s business world, effective talent management is an absolute necessity. It is the key to unlocking the full potential of a workforce, driving innovation, and ensuring long-term success. By investing in talent management strategies, private businesses can build resilient, engaged, and high-performing teams that can help them weather challenging times and propel them to new heights. Successful talent management provides numerous benefits, including:

Driving Innovation and Adaptability

Talent management is instrumental in fostering innovation within any business (AIHR). By identifying and nurturing individuals with diverse skill sets, experiences, and perspectives, companies can create a dynamic workforce capable of generating fresh ideas and adapting to changing market trends. Innovation is the lifeblood of any successful company, and a well-managed talent pool is essential for staying ahead of the curve.

Achieving Business Goals and Objectives

For a business to thrive, it is critical that employees at all levels are aligned with its strategic goals and objectives (Rizolve Partners). Talent management ensures that the right people, with the right skills, are in the right positions to drive the company forward. This alignment maximizes efficiency and improves decision-making processes. Talent management also helps you to measure and improve the performance and impact of your employees, and to identify and address any gaps or risks. By doing so, you can optimize your resources, increase your effectiveness, and enhance your profitability and growth.

Enhancing Employee Engagement and Productivity

Engaged employees are more likely to be productive, committed, and aligned with the organization’s goals (HBR). Talent management involves creating an environment where employees feel valued, supported, and encouraged to develop their skills. When employees believe in their potential for growth within the company, they are more likely to invest time and effort in their roles, resulting in increased productivity and overall business success.

Mitigating Risks and Building a Resilient Workforce

Talent management goes beyond hiring skilled individuals; it involves planning for the long term. By identifying and developing potential leaders within the organization, businesses can create a pipeline of talent capable of taking on key roles. This succession planning mitigates the risks associated with sudden departures or unexpected changes in leadership, ensuring continuity and resilience (McKinsey).

Improving Employee Retention

High turnover rates can be detrimental to the success of any business. Recruiting and training new employees incur significant costs, both in terms of time and resources. Employee turnover is a significant issue for many businesses in North America, as it can result in high costs, low productivity, and low morale. The average cost of replacing an employee can range from 0.5 to 2 times the employee’s annual salary and even more for C-level positions (Gallup). Talent management focuses on retaining valuable employees by offering career development opportunities, mentorship programs, and a positive work environment. Satisfied and engaged employees are more likely to stay with the company, reducing turnover and preserving institutional knowledge.

Enhancing Organizational Culture and Your Employer Brand

In today’s interconnected world, a company’s reputation as an employer plays a crucial role in attracting top talent (HBR). Effective talent management not only focuses on internal development but also emphasizes creating a positive employer brand. It helps you to foster a culture of collaboration, innovation, and diversity, and to align your employees with your values and goals. A company known for valuing its employees, nurturing growth, and providing a supportive work environment will naturally attract high-calibre professionals, giving the business a competitive advantage in the talent market.

CORE COMPONENTS OF A TALENT MANAGEMENT STRATEGY

A well-defined talent management strategy is the cornerstone of building a workforce that not only meets your current business needs but also ensures sustained success in the future. Some of the key components of an effective talent management strategy are:

1. Conducting a Thorough Talent Assessment

Before embarking on the development of a talent management strategy, it’s crucial to understand the existing talent within your organization. Conduct a comprehensive talent assessment to identify skills, competencies, and potential gaps. This analysis sets the foundation for targeted recruitment, development, and succession planning.

2. Aligning with Strategic Objectives

Your talent management strategy should seamlessly integrate with the overall strategic objectives of the business. Identify the critical skills, competencies, and behaviours for different roles and levels. And clearly define how the acquisition, development, and retention of talent contribute to achieving long-term goals. Identify key performance indicators that will measure the success of your talent management efforts.

3. Creating a Succession Plan

Develop a robust succession plan that identifies critical roles within the organization. Establish a talent pipeline by grooming internal candidates for key positions. This proactive approach ensures a smooth transition in leadership and minimizes disruptions caused by unexpected departures.

4. Implementing Effective Recruitment and Onboarding

Craft a recruitment strategy that goes beyond traditional methods. Leverage online platforms, social media, and professional networks to attract top-tier talent. Utilize data and technology to optimize the recruitment process and to ensure a positive candidate experience that showcases your company’s culture and brand. Include clear and consistent criteria for selecting and evaluating candidates. Once recruited, streamline the onboarding process to integrate new hires into the company culture, mission, and workflows.

5. Promoting Continuous Learning and Development

Foster a culture of continuous learning within your organization. Offer regular training programs to enhance employee skills and knowledge. Provide opportunities for professional development and career advancement, creating an environment where employees feel invested in their growth.

6. Fostering a Positive Work Environment

Cultivate a positive workplace culture that values diversity, equity, inclusion, and employee well-being. Promote open communication channels, encourage collaboration, recognize and reward achievements, and celebrate successes. A positive work environment contributes significantly to employee satisfaction and retention.

7. Implementing Performance Management and Feedback Mechanisms

Establish clear performance expectations and goals for employees. Empower your employees to make decisions and take ownership of their work, and provide them with autonomy, support, and the resources required to achieve their objectives. Implement regular performance reviews and feedback mechanisms to track progress. Provide constructive feedback and support for employees’ professional growth to ensure a continuous improvement mindset.

8. Creating a Culture of Employee Engagement and Retention

Regularly gauge employee satisfaction through engagement surveys. Address concerns promptly and implement retention strategies, such as career development opportunities, flexible work arrangements, and competitive compensation packages. A satisfied and engaged workforce is more likely to stay committed to the organization.

9. Offering Competitive and Fair Compensation

Provide compensation and benefits that are attractive and meaningful for your employees. Compensation and benefits should be based on market research and benchmarking and should be linked to the performance and potential of the employees, reflecting their contribution and value to the organization.

10. Staying Agile and Adaptable

Recognize that the business landscape is constantly evolving. Periodically review and update your talent management strategy to stay aligned with changing business needs. Being agile and adaptable ensures that your strategy remains relevant and effective over time.

Developing a robust talent management strategy is a critical investment in the future success of your business. By conducting thorough assessments, aligning with strategic objectives, and implementing effective practices, you can build a talented, engaged, and resilient workforce that optimizes your human capital, enhances your organizational performance, and propels your organization toward sustained growth and prosperity.

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth. To learn more, check out our services here.

Recessionary times can be challenging for any business, but they also present opportunities to improve efficiency, innovation, and customer loyalty. There are strategies that business owners can adopt to not only survive but also ultimately thrive. Here are some ideas to help you prepare for and manage your business during challenging times:

Manage your costs and expenses:

With inflation and competition high, you need to be smart about how you spend your money. Streamline processes to reduce waste and improve operational efficiencies. Review and cut non-essential expenses without compromising quality. Renegotiate contracts with suppliers, vendors, and landlords to secure better terms.

Stop doing what isn’t working and clean house of non-core assets:

Stop selling unprofitable lines. Stop doing marketing that is not working. Stop subscriptions that are not being used. File taxes on time and stop the penalties. Sell land and buildings that are not used well in the business. Sell parts of the asset portfolio that are non-core. Dismiss unproductive employees. Identify loss-making client accounts, that require too much sweat equity, or are problematic and a drain on resources that can be put to better use elsewhere.

Analyze and manage your cash flows:

You need to have a clear picture of how much money is coming in and going out of your business, and how that might change in different situations. Expedite customer payments by instituting a process of timely collection of receivables; for new accounts ensure reasonable collection periods of 30-45 days; do credit checks for new accounts and slow payers. You can also increase your cash flow by reducing your inventory levels and clearing your stock as fast as possible. Cash flow forecasting tools can help you create realistic and flexible scenarios, and by identifying the key drivers and risks of your cash flow, you will be in a better position to plan and manage accordingly.

Build cash reserves and review your finance options:

Having enough cash on hand can help you weather the storm and take advantage of new opportunities. It’s prudent to have at least six months of business expenses saved up to ensure your business can cope with a slump. Examine your cash reserves and if you feel you may have difficulties, look for options to extend and defer your debt. Explore funding options and establish lines of credit in advance. Ask for a discount for immediate payment. Find additional creditors with better terms. Consider alternatives like grants and loans. Invoice factoring is another option that can provide you with cash right away by selling your invoices to a company that will recover the money owed.

Prioritize customer satisfaction and retention efforts:

Your customers are the reason you are in business, and you need to retain their trust and loyalty. Encourage customer feedback and use it to make necessary or opportunistic adjustments. Consider offering additional value or services to retain customers during tough times. You can reach out to them through various channels, such as email, social media, or phone, and provide them with valuable information, offers, and support. Make the effort to understand your customers’ changing needs, preferences, and pain points so that you can tailor your products or services as well as your selling propositions more effectively.

Keep your employees in the loop and manage their wellbeing:

Your employees are your most valuable asset, and you need to keep them motivated, engaged, and productive. Focus on retaining key talent. Communicate with them regularly, share your vision and goals, and solicit their feedback and ideas. Consider offering them professional development opportunities, flexible work arrangements, and wellness programs to support their health and well-being. Cross-train employees to broaden or deepen their understanding of the business as well to enhance flexibility and adaptability within your organization.

Ensure your operations are lean, streamlined, and agile:

You need to be able to adapt quickly and efficiently to changing market conditions and customer demands, particularly in tough times. To do that you need to understand and look for ways to improve the performance of all of your business investments. For example – your investment in people: Is your headcount optimized? Are each of the heads performing? Who could you lose if you needed to? Is your investment in advertising and promotion paying off? Are you attracting the right target audience and is the ROI satisfactory? Are there areas of spending that should be stopped or reallocated? What about your capital investments? Are planned capital expenditures necessary? Are they out-of-pocket? Could you subscribe monthly instead, or could you take on asset financing? Finally, is your investment in working capital well managed? It’s always important to look for ways to lower your receivables and inventory and to stretch your credit.

Invest in digital transformation and innovation:

Technology can be a tremendous ally in a recession because it can help you improve your performance, reach new markets, and create new value propositions. Consider implementing automation and technology solutions to enhance productivity and reduce costs. You can use digital tools to enhance your online presence, optimize your marketing campaigns, and analyze your data to inform your strategies and tactics. Digital technologies that can improve the customer experience, as well as your operational efficiency, can be very wise investments that deliver high returns.

Explore opportunities to diversify:

Diversification can help reduce the risk of relying on a single product, service, market, or industry. By spreading their investments across a range of different areas, businesses can protect themselves against market downturns, changes in consumer preferences, or other external factors that could impact their existing operations. Diversification can also enable businesses to take advantage of new opportunities, achieve economies of scale, and increase their profitability. Explore opportunities to diversify your company’s product or service offerings to appeal to a broader market. Also, consider entering new markets or expanding your geographical reach.

Establish strategic partnerships:

Strategic partnerships can be a powerful way to grow your business and survive in challenging times. Seek strategic partnerships, joint ventures or alliances that can provide mutual benefits and help weather economic challenges. For example, by collaborating with partners that offer complementary products or services, you can access new customers and markets, generate more income, and mitigate risks. Partnerships can also help reduce costs, improve efficiency, and drive innovation by pooling together resources and expertise. Partners can help each other overcome challenges and gaps in their capabilities as well as help each other differentiate their brands and create more value for customers. Forming strategic alliances may enable you to gain an edge over your competitors and increase your market share in both good and tough times.

It’s important to remain adaptable and responsive to changing market conditions. By focusing on the areas discussed above, you can enhance the resilience of your business during challenging economic times and position your company for long-term success. If you have surplus cash then consider investing for the future in people, systems, processes, new product development, research, and planning.

Rizolve Partners is a key asset in helping business owners create a plan for growth and liquidity. To learn more, check out our services here.

Recently we talked about the key competencies of an effective Marketing Plan and Sales Plan – two essential components of any business strategy. They outline the goals, strategies, and tactics for creating awareness, generating leads, and converting prospects into customers. However, to achieve optimal results, these plans need to be aligned and integrated.

WHAT IS AN INTEGRATED SALES AND MARKETING PLAN?

An integrated sales and marketing plan is a document that describes how the marketing and sales teams will work together to achieve the business objectives. It defines the roles and responsibilities of each team, the processes and tools they will use, the metrics and targets they will track, and the incentives and rewards they will receive.

THE BENEFITS OF AN INTEGRATED SALES AND MARKETING PLAN

An integrated sales and marketing plan is a strategic approach that aligns the goals and activities of the sales and marketing teams to achieve better results. For example, it can help to:

Improve your understanding of the target audiences: By combining the insights from both teams, you can get a better understanding of your target audiences. Marketing can see what content and channels attract and engage your prospects, while sales can see what pain points and goals motivate them to buy.

Create a consistent and coherent message across all channels and touchpoints: By having a clear understanding of the target market, the value proposition, and the buyer journey, the sales and marketing teams can craft and deliver a unified message that resonates with potential and existing customers. This can increase brand awareness, trust, and loyalty, as well as reduce the confusion and inconsistency that may arise from different messages.

Improve the quality and quantity of leads and opportunities: By collaborating and sharing data and insights, the sales and marketing teams can generate more qualified leads and nurture them effectively through the sales funnel. The marketing team can create relevant and engaging content and campaigns that attract and educate the prospects, while the sales team can provide timely and personalized follow-up and feedback that move them closer to the purchase decision.

Increase the conversion rate and shorten the sales cycle: By having a common definition of the ideal customer profile, the lead scoring criteria, and the sales readiness indicators, the sales and marketing teams can ensure that only the most qualified and ready leads are passed from marketing to sales. This can reduce the wasted time and resources on unqualified or uninterested leads and increase the chances of closing the deal faster and more efficiently.

Enhance the customer experience and increase satisfaction: By providing a seamless and consistent experience across the entire customer journey, the sales and marketing teams can delight and retain the customers. The marketing team can continue to provide valuable and relevant content and offers that increase customer engagement and loyalty, while the sales team can provide proactive and responsive support and service that addresses customer needs and pain points.

Reduce the cost of acquisition and retention: By working together and leveraging each other’s strengths and resources, the sales and marketing teams can optimize the return on investment and lower the cost per lead and cost per customer. The marketing team can use data and analytics to measure and improve the effectiveness and efficiency of their campaigns and channels, while the sales team can use automation and personalization to streamline and enhance their processes and interactions.

Boost revenue and profitability: By achieving the above benefits, the sales and marketing teams can ultimately increase the revenue and profitability of the business. The integrated sales and marketing plan can help to generate more leads, convert more customers, increase the customer lifetime value, and reduce customer attrition.

HOW TO INTEGRATE YOUR SALES AND MARKETING PLANS

To create an effective integrated sales and marketing plan, you need to follow a systematic process that involves the following steps:

1. Define your target market and buyer personas. Identify who your ideal customers are, what their needs and pain points are, how they make buying decisions, and where they can be reached.

2. Develop your value proposition and positioning statement. Your value proposition is the unique benefit that your product or service offers to your customers. Your positioning statement is how you want your customers to perceive your brand in comparison to your competitors. These statements should be clear, concise, and compelling, and should be communicated consistently across all channels and touchpoints.

3. Choose your marketing and sales strategies and tactics. Based on your target market, buyer personas, goals, objectives, value proposition, and positioning statement, decide on the best mix of marketing and sales activities to reach and engage your prospects and customers. For example, you may use content marketing, email marketing, social media marketing, SEO, PPC, webinars, events, etc. for marketing, and cold calling, referrals, demos, proposals, negotiations, etc. for sales.

4. Align your sales and marketing goals and metrics. The alignment of goals and metrics is crucial to ensure that your sales and marketing teams have a common vision and direction and that they are working towards the same objectives. You need to set SMART (specific, measurable, achievable, relevant, and time-bound) goals that align with your overall business strategy and define key performance indicators (KPIs) that measure your progress and success. You also need to establish a service level agreement (SLA) that defines the roles and responsibilities of each team, and the expectations and deliverables of each stage of the sales funnel. For example, an SLA may specify the number and quality of leads that marketing will deliver to sales, the response time and follow-up actions that sales will take, and the feedback and reporting that both teams will provide to each other.

5. Collaborate and communicate regularly between the sales and marketing teams. You need to create a communication plan that specifies the frequency, mode, and agenda of your meetings and updates, and use a shared platform or tool that allows you to exchange information and feedback in real-time. This step is vital to foster a culture of trust and cooperation between your sales and marketing teams and to avoid silos and conflicts.

6. Implement your marketing and sales tools and systems. To execute your strategies and tactics effectively, you need to have the right tools and systems in place. These include your website, CRM, marketing automation, sales enablement, analytics, etc. These tools and systems should be integrated to ensure seamless data flow and collaboration between the teams.

7. Monitor and measure your performance and results. To evaluate the effectiveness of your integrated sales and marketing plan, you need to track and analyze the relevant metrics and KPIs. These include the marketing and sales funnel stages, conversion rates, revenue, ROI, etc. You should also conduct regular reviews and feedback sessions to identify the strengths and weaknesses of your plan and make adjustments as needed.

8. Share data and insights to optimize your campaigns and processes. This step is important to leverage the power of data and analytics to improve your decision-making and performance. You need to collect and analyze data from various sources and channels, such as your website, social media, email, CRM, etc., and use it to generate insights and recommendations that can help you optimize your campaigns and processes. You also need to share your data and insights with your sales and marketing teams and use them to test and refine your strategies and tactics.

9. Provide feedback and support to each other to improve your performance and results. This step is necessary to maintain a continuous improvement cycle and a growth mindset. You need to monitor and evaluate your results and outcomes and identify your strengths and weaknesses. You also need to provide constructive feedback and support to each other and learn from your mistakes and failures. You also need to seek new opportunities and challenges and innovate and experiment with new ideas and approaches.

10. Reward and celebrate your achievements and successes. To motivate and inspire your teams, you need to recognize and reward their efforts and accomplishments. You can use various incentives and rewards, such as bonuses, commissions, recognition, promotions, etc. You should also celebrate your achievements and successes as a team and foster a culture of collaboration and trust.

THE BOTTOM LINE

Integrating your sales and marketing plans can help you create a consistent and compelling brand narrative, improve your campaign performance and customer experience, optimize your resources and costs, and increase sales and retention, ultimately grow your revenue. By aligning your goals, strategies, and metrics, and communicating and collaborating across teams, you can achieve a seamless and effective full-funnel process that adds value to both your customers and your business.

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth. To learn more, check out our process expertise tips sheets here.

When we first met our brand-new Vice President of Sales, the CEO of the company had just laid out the strategic plan to the executive team, hinging on the necessity to implement a world class sales strategy to deliver the revenue necessary to fulfill the company’s aggressive growth objectives!

No problem: In this final installment of our 3-part series examining the key drivers of successful revenue growth that create real value, we will build on the four key components of the Sales Plan (outlined in Part 2) that included:

– A documented, well-understood sales strategy;

– A defined sales process and methodology;

– Ongoing sales training and development; and

– The effective use of data analytics and readily available technology.

In this article – Part 3 of the series – we will explore what makes for a truly effective sales strategy to deliver on the company’s objectives.

Key Elements of a World Class Sales Strategy

Best-in-class companies implement sales strategies through a combination of effective planning, execution, and ongoing refinement. While specific strategies can vary depending on the industry, target market, and product or service, there are some common elements that top-performing companies tend to incorporate into their sales strategies.

Let’s explore some key aspects of how they achieve this…

Market Research:

Best-in-class companies invest heavily in market research, gaining a comprehensive understanding of their target market. This includes in-depth knowledge of customer needs, preferences, and pain points. Legendary management guru, Peter Drucker, notes that “Quality in a product or service is not what you put into it, it is what the customer gets out of it.” So, understanding your customer requirements is imperative.

They also conduct rigorous competitive analysis to identify strengths, weaknesses, opportunities, and threats. Continuous monitoring of market trends and changes allows them to stay ahead of the curve.

Clear Sales Objectives:

Setting well-defined and measurable sales goals and targets is a key component of any plan. Tracking specific Key Performance Indicators (KPIs) to measure progress and ensure that their sales objectives align with broader business goals allows for monitoring of achievements.

Customer Segmentation:

Segmentation of the customer base enables the tailoring of approaches to different customer groups to align with their needs more specifically and effectively. This involves the creation of detailed buyer personas to understand customer demographics, behaviours, and motivations, allowing for more personalized interactions.

Sales Team Training and Development:

Ongoing training and development programs are a priority. They equip the sales team with the knowledge and tools necessary to excel in their roles, ensuring they stay up to date with industry trends and product knowledge.

Sales Process Optimization:

Salespeople are quick to point out that their industry is specialized, and that you need unique knowledge and experience to be successful. Brian Halligan, CEO of HubSpot, states “In sales, it’s not about what you sell; it’s about how you sell it.”

The development of a clear and effective sales process that guides salespeople through each stage of the sales cycle is a key goal that allows for future scalability. Regular refinement and optimization of the process based on performance data and feedback ensures continued efficiency.

Technology and Tools:

Utilization of CRM (Customer Relationship Management) systems is common. These systems help manage customer information, track interactions, and automate routine tasks. Additionally, they implement sales enablement tools to provide sales teams with the right content and resources at the right time.

Fortunately, these tools are readily available and have come down in price and complexity so that any size company can take advantage of these benefits.

Sales and Marketing Alignment:

There’s a strong focus on collaboration between sales and marketing teams. Shared goals, messaging, and strategies are developed to generate and convert leads effectively. This alignment helps prevent the disconnect between the two departments which can sometimes hinder sales efforts.

Lead Generation and Management:

Effective strategies for lead generation are put in place, encompassing both inbound and outbound channels. Lead nurturing processes are established to move prospects through the sales funnel, ensuring that potential customers receive the right information and support at each stage.

Performance Metrics and Analytics:

Regular measurement and analysis of sales performance and pipeline data are integral to decision-making. These companies use data to make informed decisions and adjust the sales strategy as needed, ensuring a data-driven approach to sales.

Customer Relationship Management:

Building and maintaining strong relationships with customers is a priority. These companies provide excellent customer support and post-sales service to foster loyalty and encourage repeat business. As Sam Walton, founder of Walmart stated, “The goal as a company is to have customer service that is not just the best but legendary”.

Incentives and Compensation:

Incentive and compensation plans are designed to motivate the sales teams. They reward top performers and align compensation with sales goals, ensuring that the salesforce remains highly motivated.

Feedback and Iteration:

Best-in-class companies actively seek feedback from the sales team, customers, and other stakeholders. They continuously iterate and adapt the sales strategy based on this feedback and performance results.

In the 1970’s no company demonstrated this more than Harley Davidson, relying on key feedback mechanisms to rescue the company from near obscurity to become the iconic brand it is today. “The more you engage with customers, the clearer things become and the easier it is to determine what you should be doing.” – John Russell, President of Harley-Davidson

Risk Management:

Taking risks is a requirement in business. Mark Zuckerberg, the co-founder and CEO of Facebook maintains “The biggest risk is not taking any risk. In a world that’s changing quickly, the only strategy that is guaranteed to fail is not taking risks.”

However, world class companies identify potential risks and challenges in the sales process and develop contingency plans to mitigate risks and overcome obstacles. This proactive risk management helps to ensure a smoother sales process.

Compliance and Ethical Practices:

Making sure that the sales strategy adheres to legal and ethical standards is a discipline expected by the market. Maintaining transparency and integrity in all sales interactions is a core principle for customer success.

Implementing a world class sales strategy is not rocket science! Our new VP of Sales needs to understand that it takes discipline to deliver a comprehensive plan and that it is an iterative process. The first steps include researching client needs, setting clear objectives, and defining the target customer segments. This forms the basis for any sales plan; however the VP needs to recognize and that continuous refinement is a defining factor of an effective strategy.

Best-in-class companies remain agile and open to change, continually adjusting their sales strategies based on market dynamics and emerging opportunities. They also invest in technology, data analysis, and employee development to stay at the forefront of their industries, which allows them to consistently outperform competitors in their respective markets.

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth. To learn more, check out our process expertise tips sheets here.

You are the brand-new Vice President of Sales attending your first executive planning meeting. You swagger into the board room, seat yourself to the right of the CEO at the head of the board table (the position of power), and look around at your colleagues with the confidence that says … I belong here! And you do… you have worked hard, you have excellent credentials, you excelled as a salesperson, and you are ready to take on this new challenge!

The CEO, after welcoming you to the “adult’s” table, then proceeds to lay out the strategic plan that has been underway for 12 months, reviewing the components of the economic engine that are now in place to support a growth strategy that delivers true value to the company. The financial resources have been secured, the operational improvements have been made, the human resource plan is now in place, and the commitment to the shareholders has been made…

The CEO looks your way and announces … “and now our new VP of Sales will outline the elements of the sales strategy to get us there”! And that’s when it hits you … “I need a plan”!

This is the second of a 3-part series examining the key drivers of successful revenue growth that creates real value. In the first part, we looked at the organizational elements required to be in place to ensure that the company can deliver on the promises made by the sales department. We discussed how the resources of the company should be properly organized to deliver on the plan, to maintain balanced momentum as the revenue accelerates.

This time around, we will look at the key sales competencies that our new VP must establish to provide the fuel that will sustain the corporate strategy that represents the number one objective of 66% of all CEOs: Growth!

When it comes to the competencies of a sales team or company, the focus shifts from individual skills to collective abilities and strategies. Here are four key sales competencies that are crucial for a successful sales organization…

Sales Strategy:

A well-defined sales strategy is fundamental to a company’s success in the market. This competency involves setting clear objectives, defining target markets, segmenting customers, and determining the best approaches for reaching and engaging potential buyers. A strong sales strategy also includes pricing strategies, distribution channels, and sales forecasting.

While this sounds like “Sales 101”, it is surprising how many companies identify sales strategy as a major pain point.

89% of small to mid-size companies surveyed** indicated that they struggled to identify how they were positioned within their industry, the strengths and weaknesses of their key competitors, and even their value proposition (more than half of small to mid-size companies reported that they didn’t have a value proposition).

Of course, these are all essential elements of a successful sales strategy.

Sales Process and Methodology:

Establishing a standardized and efficient sales process is essential for consistent results and scalability. This competency includes defining the stages of the sales cycle, creating a structured approach to lead generation and qualification, and implementing sales methodologies that guide salespeople in their interactions with customers.

The sales process is a structured series of steps that a sales team follows to guide a prospect from initial contact through to a closed deal.

Simple right?

Yet only 10% of the companies surveyed stated that they have done an adequate job educating their sales teams on the essential steps.

Sales methodology refers to a systematic approach or framework that guides the sales team in how they interact with prospects and customers throughout the sales process. It provides a set of best practices, strategies, and tactics for selling effectively. Several sales methodologies exist, and organizations may choose or adapt one based on their specific needs, but we will do a deeper dive into these options in part 3 of this series.

At the end of the day, it’s about consistency in the sales process that helps ensure that sales activities are systematic, consistent, and aligned with the company’s sales strategy.

Sales Training and Development:

Investing in the continuous development of sales teams is a critical competency. Providing sales training, coaching, and mentorship helps salespeople acquire the skills they need to excel in their roles. Ongoing development programs also keep sales teams updated on industry trends, product knowledge, and sales techniques.

While this clearly would benefit the salesperson’s ability to close business (also a major bonus to the company), there is the additional benefit of building and retaining a seasoned, experienced sales force. In fact, Forbes magazine recently stated that “skills are becoming the new currency” for hiring and retention.

According to a LinkedIn Learning report, 94% of employees would stay at a company if it invested in their career development.

Data Analytics and Technology:

Michael Dell, the founder of Dell Computers once said “Our business is about technology, yes. But it’s also about operations and customer relationships.”

In today’s data-driven business landscape, companies can and must leverage data analytics and technology to make informed decisions about customers to optimize sales performance. This competency involves using customer relationship management (CRM) systems, sales analytics tools, and data-driven insights to track sales activities, analyze customer behaviour, and make data-backed decisions for improving sales strategies.

Once upon a time, these tools were expensive and limited only to those experts in the IT department with the skills to extract meaningful information from reams of data. Today, advances have made these tools cost-effective and user-friendly to the point that sales teams can effectively track customer interactions through the sales funnel, maximizing the opportunity to close business like never before.

Summary:

Let’s get back to our new VP of Sales and the challenge to develop an effective sales plan to fuel the overall company objective for sustainable and predictable growth! The good news is that sales strategy and technology have advanced to provide the roadmaps and the tools necessary to establish an effective sales strategy for any industry. The key components include:

A documented, well-understood sales strategy

A defined sales Process and methodology

Ongoing sales training and development

The effective use of data analytics and readily available technology

These four competencies work together to create a strong foundation for a successful sales organization. A well-defined sales strategy informs the sales process, and ongoing training and technology enable sales teams to execute that strategy effectively. Additionally, continuous evaluation and adjustment of these competencies are essential to stay competitive in a dynamic marketplace.

Finally, the effective implementation of these strategies is proven to generate positive sales results that meet corporate objectives and allow our VP of Sales to maintain that confident swagger!

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth.

To learn more, check out our process expertise tips sheets here.

Two-thirds of CEOs state that their number one corporate objective is to grow the company. For many, growth is defined by increasing Sales Revenue.

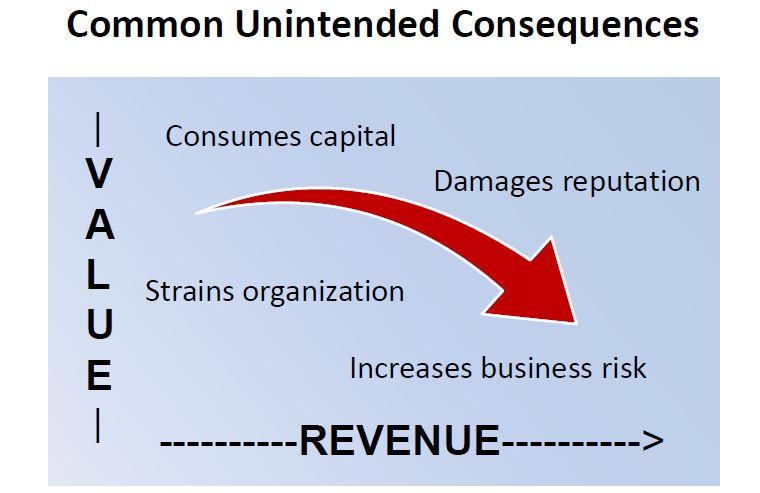

But how many times have you witnessed companies on a tear that experience unintended issues which end up being terminal for the same CEO who mandated the growth?

By stepping on the accelerator and increasing sales, the company may have inadvertently created an even bigger problem than anaemic growth.

Some examples of unintended consequences that impact other value drivers in the company and potentially destroy value include:

This is the first of a 3-part series that examines the recipe for success that delivers increased value associated with certain types of Sales Revenue growth – …the golden nugget that you have been looking for – Value acceleration.

In this first part, we’ll examine the essential components of the economic engine necessary for the achievement of a successful revenue growth strategy that delivers value. By successful we mean that the revenue achieved needs to be predictable and sustainable. In the next two parts of the series, we will be discussing the “What” and then the “How” (stay tuned – they are the important bits).

The first question that my Sales Xceleration expert partner always asks when we talk about growing a company is “What is the $ Goal we want to achieve?”. This is the right question. We want to grow – but you need to answer the question: by how much and how quickly? In other words, he is asking the question “What is the Plan?”.

The plan goals should be both Strategic (3-5 years out) and Tactical over the shorter term (typically one year). Strategic goals are necessary because building out a sales team with tools, systems and processes that are scalable are long-term activities that require investment capital. Tactical goals targeting a certain level of sales once the infrastructure is in place with the appropriate skills, require a further level of detail to prove that the revenue levels contemplated provide a satisfactory return on investment.

Importance of a Business Plan

A written business plan is a statement of intent and clarification of purpose for everyone involved. It is a clarification of priorities. At its simplest, it is a communication tool and the golden key to fostering buy-in and alignment. For the team involved in implementing the plan, it is also a motivational tool as they can begin to envisage their role in executing the plan.

A planning process allows for kinks in the thinking to be ironed out minimizing the bumps in the road and therefore allowing for acceleration to occur. It provides a methodology for ideas and assumptions to be proved. It is a GPS that gives you a road map to reduce the odds of getting lost along the way. In other words, it is a risk-reducing exercise.

Fundamentally, it allows targets and goals to be set that can be benchmarked for reasonableness, and ceiling tested against company capacity and achievability. Crucially, it provides analytical support to aid critical decision-making and reduce guesswork.

Put in the context of the question: “What is the sales goal you want me to plan for?” it provides a process to answer the question: “At a particular level of sales and velocity, does the organization’s operations have the capacity, process, and competency to deliver on the promises made by the sales department”.

What Disciplines are a Prerequisite to Reliably Deliver Sales Revenue Growth?

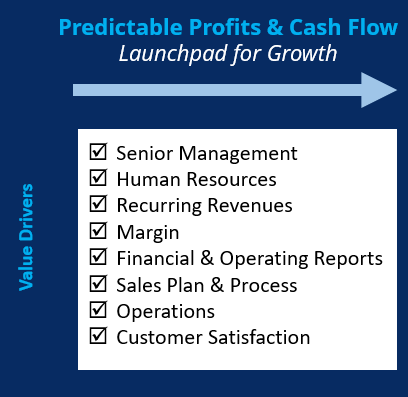

Growth that is valuable needs to be sustainable, predictable, and transferable into the hands of a third party. It also follows that as value increases so does the ability to deliver higher levels of profitability and cashflows. The disciplines that are required as a foundation to deliver such results are:

Senior Management provides leadership and planning to decide on goals; clarify priorities and make decisions on the allocation of resources. Management provides the conditions under which alignment and motivation can be fostered toward the achievement of goals.

Human Resources create and develop the skills and knowledge base needed for the company to execute its goals.

Recurring revenues allow the company to sustain its operations, providing the predictability for the company to pay its bills as they fall due and to invest for future growth. Recurring revenues have a higher value than one-off gains for these reasons.

Margin is the ability of the company to make an economic return on its activities. The higher the margin relative to the industry average the more valuable the company is compared to its competitors.

Financial and operational reports allow the company to monitor its progress and benchmark itself against its competitors. Timely reporting provides the key metrics that can facilitate corrective action and capture opportunities as they arise.

Sales plan and process are critical elements to organizing resources around an action plan, scaling resources around a process that is replicable with the ability to delegate, monitor, incentivize and organize.

Operations is the body of resources, tools and processes that are required to deliver on the promises made by the Sales team in a timely manner.

Customer satisfaction is the mindset of the customer after receipt of the product or service which was promised by the company. A high level of customer satisfaction is correlated with increased company value.

In short, a valuable company creates a plan to capture the economic returns from market participation and delivers returns from its activities that are higher than its competition while providing products or services that are in demand at service levels that deliver above customer expectations.

Sales Revenue Growth

Valuable sales revenue growth therefore has a business underpinning that spans each of the above disciplines. Management is responsible for deciding on the sales targets that they want to be achieved to earn a targeted rate of return, and they are responsible for putting in place the resources that are capable of delivering on each of the above business needs. Specific examples of these are:

Sales plan that has adequate work resources to achieve execution;

Financial Plans that prove the company is properly financed through the growth period;

Human resources that are skilled, trained and in place to execute using the tools at their disposal;

Pricing mechanisms that cover costs with an adequate return to cover the investment and make a reasonable economic return for the investor;

Customer service data that measures the satisfaction of the service levels being provided; and

A sales process that measures sales activity and minimizes lead management timelines.

Earning the Right to Grow

It is important in business to understand that there are various rights of passage. Sustainability and predictability are two of those rights. Sales Revenue growth fuels the prospects of a company to be valuable, but only if the prerequisites detailed above are in place and organized such that predictable profits and cash flows, at levels at least commensurate with the competition, are being earned while satisfying the customer base. In the absence of a balanced economic engine, unintended consequences occur that are costly and time-consuming to resolve.

The right of passage that allows a company to achieve valuable growth can be witnessed most clearly by growth that perpetuates when the value drivers that we have identified are balanced, working in harmony and appropriate for the size of the company in question.

This balance is what makes the difference between a successful entrepreneur and an underperforming or failing one. It is the X-factor… Different stakeholders know it when they see it; they want to be part of it when it is working and stay away from it (or leave) when it is not.

Finally, right of passage requires sustainability and predictability. In its absence, investors turn away from companies that cannot deliver on what they have promised or, at least, charge significantly higher premiums for the uncertainty. “Under promise and over deliver” is a way to successfully manage the “right of passage” that the business community demands.

Summary

In order to deliver valuable growth from Sales Revenue acceleration, it is essential to organize resources in a manner that enables the fulfillment of commitments made by the sales department. Not having the resources properly organized will lead to unintended consequences which will increase the cost of investment and extend the timeline to success, or worse cause the company to stall or fail.

Having your valuable resources in place will give the organization’s economic engine the horsepower to gear up and respond smoothly when the growth accelerator is pressed by the leadership group. We have outlined for you, above, the essential requirements of balanced growth.

In Parts 2 and 3 of this series, we will outline for you the build-out of the 4 key sales competencies that will enable you to accelerate your sales revenue growth, assuming that your economic engine is in place. We will then detail how those competencies operate in practice for “best in class” companies to deliver on your growth imperative and to sustainably achieve your right of passage to the “next level” of business value.

Rizolve Partners understands what needs to be done to achieve sustainable, high-quality growth.

To learn more, check out our process expertise tips sheets here.

Vanessa Grant is a leading corporate lawyer with Norton Rose Fulbright Canada who is skilled in preparing for and executing business transactions for entrepreneur-led private and public companies.

PLANNING YOUR BUSINESS EXIT

There are many areas in your Business Exit where agreements and representations are made to a third-party buyer that he/she will rely on in agreeing to the transaction. Having legal advice to ensure that reasonable bargains are made such that options for recourse are limited by reasonability is important to mitigate risk.

Seeking early strategic advice, followed up by disciplined pre-due diligence planning is key to negotiating a successful transaction and ensuring that momentum in the deal is preserved.

Finally, having a skilled M&A lawyer to negotiate your side of the bargain who understands the current market for appropriate legal terms, conveys to the bidding team that you are serious about concluding a satisfactory deal.

Legal Advice on Planning Your Business Exit

The legal advisor is one of the key advisors to a business owner in planning for and executing an exit. This advisor should be part of your core transition team. Their role has the key objective of ensuring that all of the existing company legal agreements and corporate governance structures are drafted and allow for a transaction to proceed with minimum friction from any stakeholder, including the buyer.

There are two core roles that the legal advisor fulfills in this regard:

Ensuring that a company is ready from a legal perspective to navigate the transaction process. This includes ensuring that the existing (and subsequent) legal agreements and corporate governance structures (controls, policies, and guidelines) are drafted in contemplation of a future purchase and sale agreement such that documented acceptance of a transition into third party ownership has been reached, so far as possible, well in advance of a transaction; and

The legal advisor has well developed experience in drafting and negotiating a purchase and sale agreements at current market terms. Not all advisors have equal experience and a legal representative who is active in the M&A market is important.

STRATEGICALLY PLANNING A TRANSACTION

In strategically planning a transaction, a legal advisor should be included to offer advice in the review in such matters as:

Tax efficiency of the ownership or corporate structure;

Capital structure and the approval process for a transaction;

The nature and extent of the liabilities contained in the financial instruments held;

The corporate governance in any shareholder agreements, the articles and the laws of the company that will impact the ability of the entrepreneur to affect a transaction;

Understanding the nature of the outcomes of different exit options.

After making a decision to transition the ownership of the company into different hands, the legal advisor should then be engaged to review, from a tactical perspective, all of the elements of the corporate group structure, agreements governing the rights of shareholders, equity compensation plans and other financial instruments, the articles of the company, the laws and existing legal agreements to ensure that there are no blockers or issues of significance that would cause a problem for the transaction. Examples of the legal counsel review would include the following:

Buy-Sell Agreements

Are there any?

If so, do these agreements contain documented purchase options?

If so, are there any provisions related to the departure of the entrepreneur?

Participation Agreements

Are there bonuses or distributions on exit?

Are there allocation of profits, distributions or carried interest that activate on sale?

Intellectual Property

Does the company have an inventory of its registered and unregistered intellectual property? For example:

Patents

Trademarks

Trade secrets

Copyrights

Domain names

Data

If the company develops or has developed its own software, is the software subject to an open-source license?

Is it clear who owns the intellectual property?

Distinguish between employer, employee, contractor or prior employer

Are protections in place to further guard the intellectual property such as:

Assignment of intellectual property agreements

Confidentiality agreements

Prior restrictions

Internal policies and procedures

Licenses

Financial Agreements

What are the financial covenants?

Are there personal guarantees that will need to be released on closing?

What are the change of control provisions?

Contracts

For all agreements:

Is there a change of control provision that requires the consent of the counterparty on a change of control (sale) of the company?

Are there limitations of liability or unlimited liability?

Are there indemnification clauses?

Do you have insurance to cover the indemnification provisions in the agreement?

Customer and vendor agreements

Is it clear which form of agreement takes precedence (look for terms and conditions that are incorporated by reference into purchase orders – do they conflict with the master agreement)?

Are the performance terms of the contract clear?

What are the termination provisions? Is the contract a long-term contract, or a short-term contract? Is the duration of the contract consistent with industry norms?

Leases

Leases almost always have a change of control provision – consider the relationship with the landlord and whether there will be any issues obtaining consent for a change of control.

Licenses

Review intellectual property clauses: who owns any intellectual property?

Human Resources

If there are any written employment agreements or offers of employment, do they reflect the current state of employment law?

What are the liabilities for vacation pay, potential severance pay, and benefits? Are these clearly documented?

Non-compete, non-solicit, confidentiality, and assignment of intellectual property provisions – what are they and what do they affect?

Retention – do you intend to provide retention incentives for any employees – all or key only?

Business Litigation and Risk Management

Litigation

Is there any litigation?

If so, is it likely to settle or be resolved prior to any sale of the company?

If it is not likely to be resolved prior to a sale, discuss with your legal advisor how best to manage it with a prospective buyer.

Reducing likelihood of litigation

Do you regularly perform credit and background checks?

Are there onerous contract terms that should be flagged for prospective buyers?

Insurance

What insurance policies are in place?

What is the scope of the insurance? Does it cover the operations of the business?

Do you need directors’ and officers’ insurance?

Does the company have CGL and named insureds?

Are professional liabilities covered such as errors and omissions?

Is workers’ compensation and employer liability covered, either statutorily or with policies?

Do you have cyber security insurance?

Do you have employee dishonesty coverage?

Corporate and Regulatory Filings

Have all the annual returns been made and are they in good standing?

Have all extra-provincial registrations been made?

Are all required regulatory and tax filings up to date in each jurisdiction in which the company does business?

Does the company have all permits in all jurisdictions to carry on its business?

Minute Books

Do you have them completed?

Are they up to date?

Is the list of shareholders up to date and accurate?

DRAFTING THE TRANSACTION AGREEMENTS

The second major area where you will need skilled legal expertise to help you mitigate transaction risk is in drafting the transaction agreements. Key documents and components of the agreement of transaction terms are:

Letter of intent (“LOI”). An LOI is a non-binding letter of intent usually drafted by a prospective buyer as an indication in writing of a buyer’s willingness to purchase the company. While the document is of a legal nature, however, it is not intended to be fully binding. The only binding obligations tend to be with respect to confidentiality and exclusivity. The LOI sets out the terms of the acquisition process and provides insight into what the final offer and its terms might look like.

Purchase and sale agreement. A buyer may elect to purchase the shares of a company or all or some of the assets of a company. The form of transaction (share or asset sale) depends on a number of factors, including tax and business risk. Regardless of the form of acquisition, a business purchase and sale agreement is a legally binding contract that outlines the terms and conditions of buying or selling the business. It specifies the purchase price, assets, liabilities, warranties, any purchase price adjustments, and other important details to protect the interests of both the buyer and the seller. Much of the negotiation of a purchase and sale agreement is around what is the limit to how much a seller has to pay where there is a breach of the representations, warranties, and covenants made. The limit might be an amount equal to the purchase price (not as common as it once was) or a percentage of the purchase price and any holdback or escrows of the purchase price.

Documenting and negotiating representations and warranties. Representations and warranties in a business purchase and sale agreement are statements made by the seller about the condition and status of the business being sold. These statements cover various aspects such as financial information, legal compliance, contracts, intellectual property, and other relevant details. If any representation or warranty is found to be untrue, the buyer may have legal remedies or options for recourse.

FINAL TAKEAWAYS

In summary, having a legal advisor with the appropriate M&A skills involved in the early consideration of the transaction strategy can save a lot of time and money. As part of the aligned core transition team, this advisor creates the potential for the transaction to proceed with minimum friction from any stakeholder, including the buyer. You can see from the above analysis that there are many areas to consider and having a trusted, knowledgeable legal advisor who knows you and your goals is critical to achieving a satisfactory outcome.

For more information about Exit Planning, check out our process expertise tips sheets here.

Book an Appointment with Rizolve

"*" indicates required fields

How to Increase Revenue

A strong sales infrastructure is key to increasing revenue and cash flows, and only 1 in 10 small and mid-size companies have one. Having the right sales strategy, tools and resources makes all the difference in setting up a successful sales program. We help businesses create record-breaking sales. Our approach is based on industry best practices with a focus on predictability, repeatability, and scalability. We identify and help implement the core sales infrastructure components needed to boost your sales revenue. Our trusted advisors have the proven, hands-on expertise to accelerate your revenue growth.

Confidently demonstrating that business performance is both repeatable and scalable is essential to achieving peak value. We bring together all the right skills, leadership, and experience to deliver the roadmap required to maximize the value of your business. Our multi-dimensional team will introduce proven methodologies to improve the value of your business by focusing you on the key value drivers that investors and acquirers look for. You can count on our expertise and ongoing weekly support to guide you through to fruition.

Confidently demonstrating that business performance is both repeatable and scalable is essential to achieving peak value. We bring together all the right skills, leadership, and experience to deliver the roadmap required to maximize the value of your business. Our multi-dimensional team will introduce proven methodologies to improve the value of your business by focusing you on the key value drivers that investors and acquirers look for. You can count on our expertise and ongoing weekly support to guide you through to fruition.